The evolution of money transfers in the US

P2P apps have become Americans' go-to money transfer method for two key reasons: speed and convenience.

When Paypal launched, in the late 1990s, bank transfers could take up to five business days to reach the recipient. By contrast, Paypal and the other P2P apps which followed made it possible to transfer money within hours, if not minutes, using just the recipient's email or phone number.

Things have changed considerably since those early days.

In 2016, ACH introduced same-day payments, bringing bank transfers on par with P2P apps. And, in 2017, Bank of America, Truist, Capital One, JPMorgan Chase, PNC Bank, U.S. Bank, and Wells Fargo created their own P2P app — Zelle — which is now used by 36% of Americans.

But the biggest turning point was FedNow. Launched in 2023, FedNow is the US version of the UK's Faster Payments network and the EU's SEPA Instant network, enabling consumers to make bank transfers within seconds, twenty-four hours a day.

The US money transfer market in 2024: What does our data tell us?

To find out, we used FinTech Insights to evaluate banks, credit unions, and neobanks' web and iOS offerings in two main categories:

- P2P transfers

- Account number zelle

- Zelle P2P (using phone or email)

- In-house P2P

- Wire/ACH transfers

Our sample consisted of 68 firms: 18 national banks, 11 regional banks, 16 credit unions, and 23 neobanks.

Zelle P2P for the win

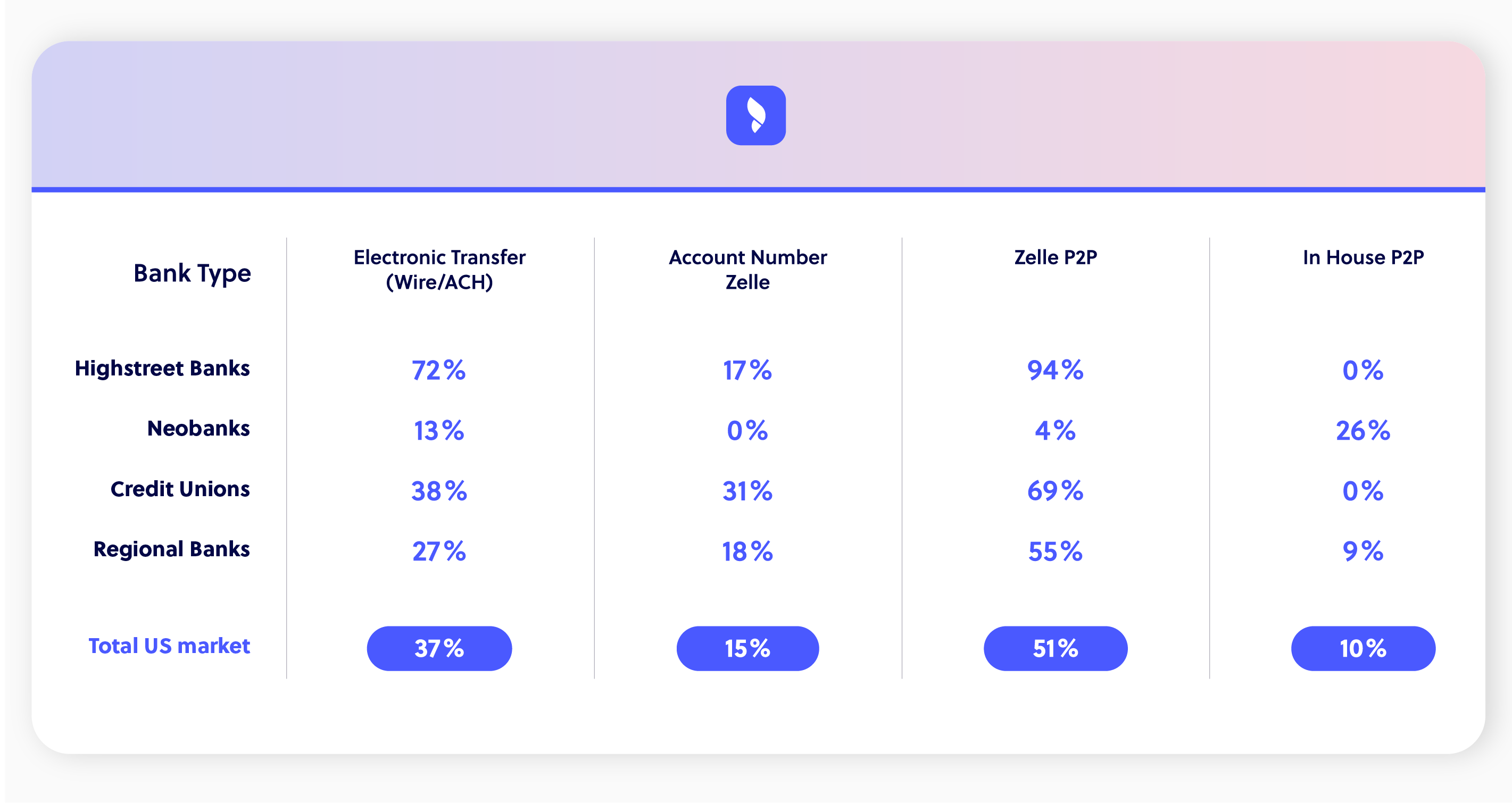

The most popular P2P payment functionality is Zelle, with 51% of our sample having the capability. And, surprisingly, traditional firms are outpacing neobanks.

With the exception of American Express, all the legacy banks in our sample offer it. 69% of credit unions also offer it, and so do 55% of regional banks.

Neobanks with Zelle P2P capabilities, on the other hand, are a rarity. The only one in our sample to offer it was Discover.

In-house P2P and account number Zelle

You'd think Zelle P2P isn't common among neobanks because many have their own in-house P2P functionality. That is, they've opted to build their own P2P infrastructure instead of integrating a third-party service.

But while more neobanks offer in-house P2P than traditional firms — no legacy banks or credit unions offer the capability, and only one regional bank, Elevault, does — it's not as common as you'd expect. Only 6 of the 23 neobanks (26%) in our sample offer it.

Zelle P2P using an account number is unpopular across the board, with only 5 credit unions (31%), 3 legacy banks (17%), 2 regional banks (27%), and no neobanks offering it.

Given that an email address or phone number is typically easier to remember than an account number, it's no surprise that account number Zelle hasn't caught on. It's also interesting to note that firms that do offer account number Zelle don't usually have ACH/ wire transfer capabilities, which suggests they're using account number Zelle as an alternative to it.

Wire/ACH trails in third place

Wire transfer technology dates back to 1872, when Western Union became the first firm to offer the service. As a highly established, familiar, tried and tested technology, you'd expect it to be widely available. And, yet, only 37% of the firms in our sample have the functionality.

At 72%, legacy banks dominate the space.

Among the rest of the firms we looked at, implementation is low across the board: it's offered by 6 credit unions (38%), 3 regional banks (27%), and 3 neobanks (13%).

Wrapping up: It's still all to play for

With Americans transferring $4.3 million a day in 2023, you'd think the market would strive to make the process as easy as possible. But our data suggests firms, including neobanks, still have work to do.

Recent developments, particularly FedNow — according to the Federal Reserve, 86% of businesses and 74% of consumers used the service in the first year since it launched — will no doubt impact the landscape as consumers become more familiar with them and warm up to their benefits.

Until then, it looks like P2P apps will keep winning all the gold.

Want to evaluate the money transfer functionality in the US digital banking market in greater detail?

Try FinTech Insights, free, today

Build a digital banking strategy that can't be challenged

Let's show you how FinTech Insights can help you wow your customers, on every login.