The chatbot explosion

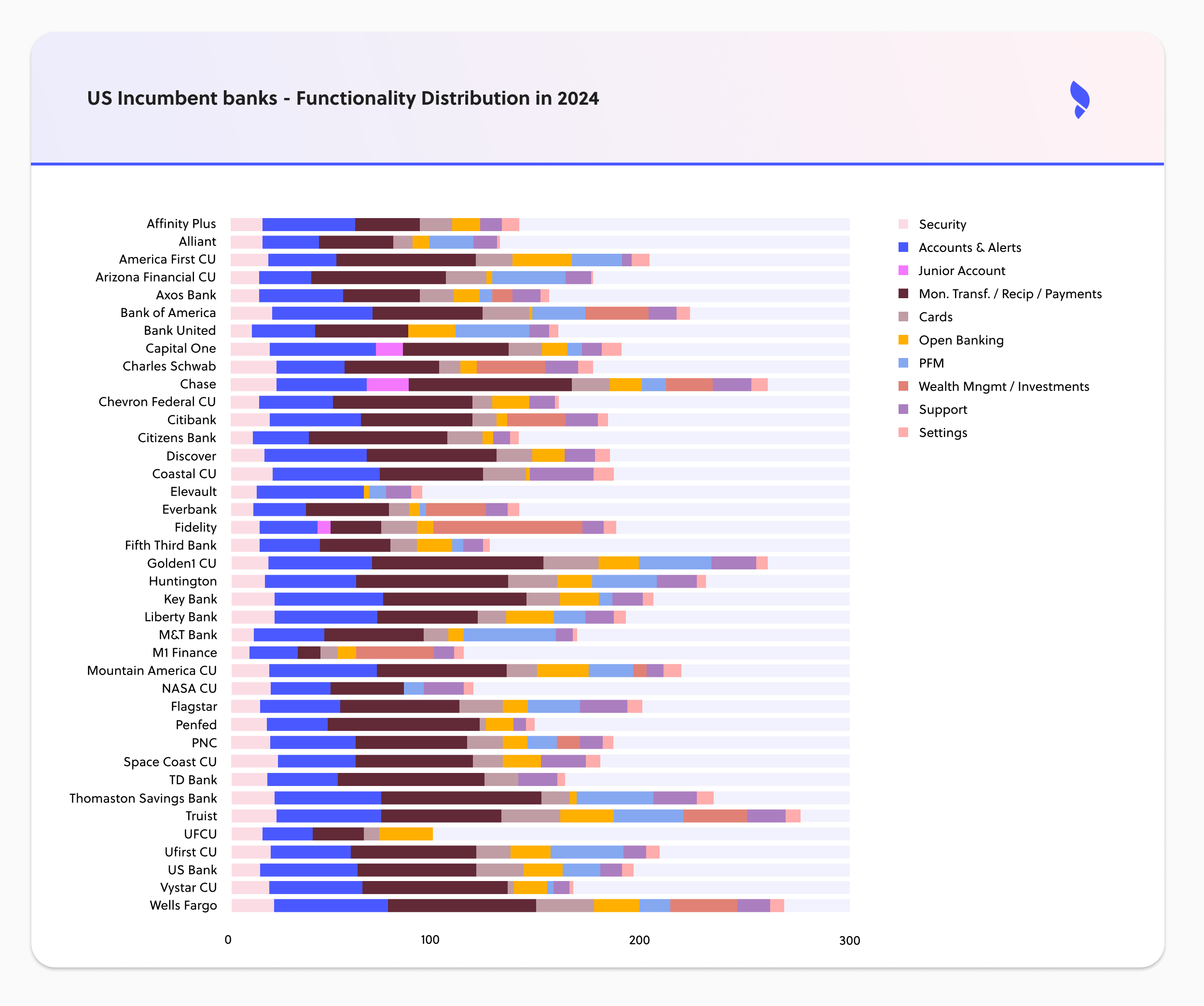

Support is the only category where every bank in our 2024 data-set — with the notable exception of UFCU — offers some functionality.

If anything, every incumbent from our 2022 dataset has increased their support capabilities, with Truist, increasing the support functionalities to 20, compared to 7 in 2022.

ChatGPT is undoubtedly part of the reason for this. Since taking the world by storm in November 2022, banks have been experimenting with it in a range of scenarios, with a particular focus on customer service.

But, market expectations are changing, too.

78% of US customers prefer to bank online, either through an online portal or mobile app. And 76% expect businesses, including banks, to offer some form of online self-service support.

The upshot is that chatbots — once a fancy nice-to-have — have been normalized. And if your customers can't sort out basic issues without leaving your app or online portal, you're at a disadvantage.

A race to stand out

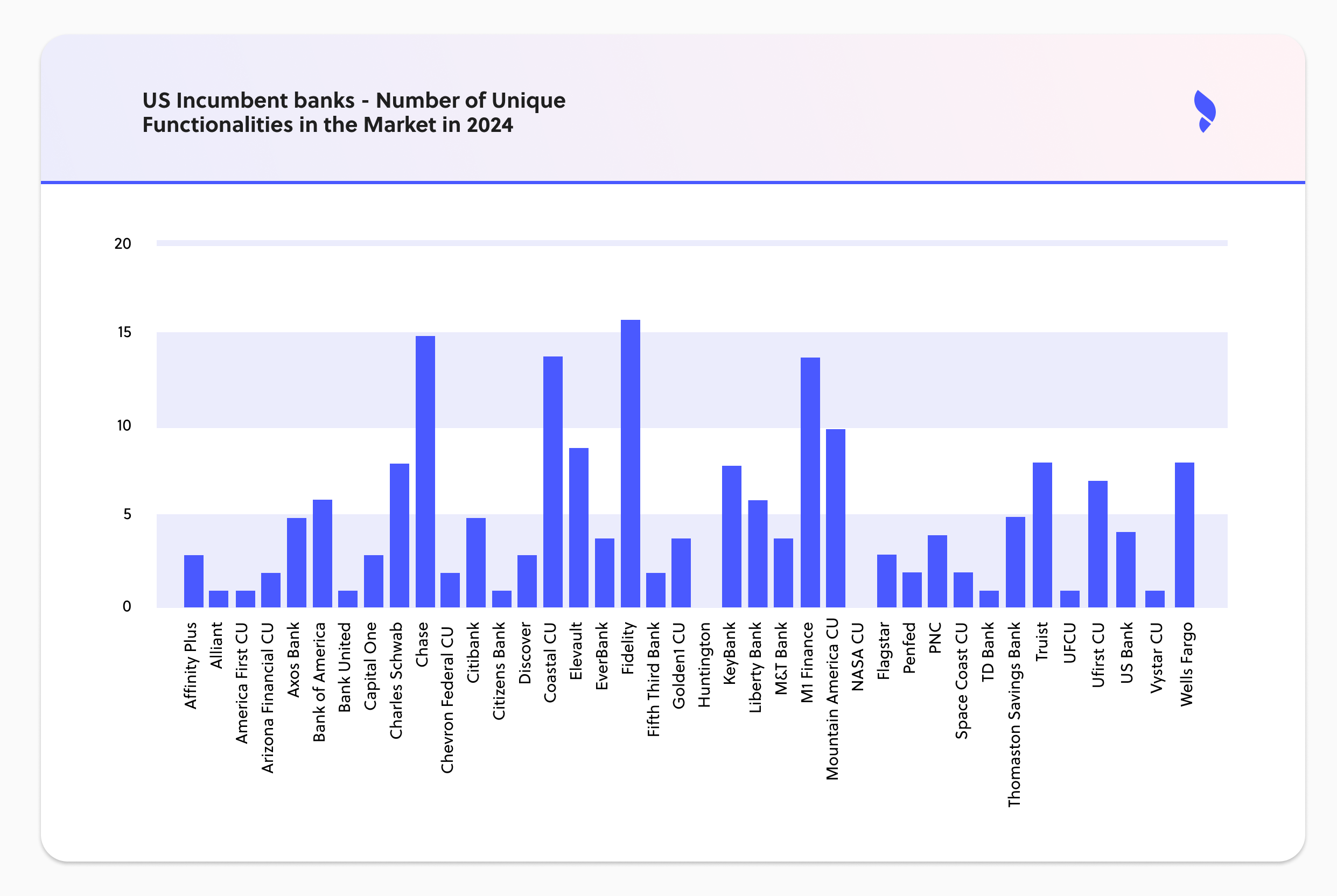

Alongside the importance of digital support, the other surprising finding in our 2024 data is a spike in unique features.

In 2022, while some banks were more feature-rich than others in certain categories, they were, by and large, almost indistinguishable from each other. The majority, 14 out of 22, had identical or highly similar products.

The landscape looks radically different in 2024, with only 1 out of 39 incumbents — NASA credit union — having no unique features.

Wells Fargo, the most differentiated incumbent in 2022, has fallen behind. It has 8 unique features, 7 fewer than it had two years ago, and is firmly in the middle of the pack. The most differentiated offerings now belong to Fidelity, Chase, and M1, with 16, 15, and 14 unique features respectively.

Differentiation in action:

Is the rise in unique functionality moving the needle when it comes to meeting market needs?

Despite some incumbents beefing up their capabilities in 2024, wealth management and junior accounts capabilities remain conspicuous by their absence.

In 2024, 11 out of 39 incumbents offer no wealth management capabilities, around the same number as in 2022.

The majority have actually decreased the number of functionalities they offer. Only four — Fidelity, Chase, Everbank (former TIAA), and Truist — have increased their capabilities.

In junior accounts, the situation is similarly unchanged.

Chase and Capital One have increased their capabilities, while Fidelity still offers the same number of features. But, 32 out of 39 incumbents offer no junior account functionality at all.

US banks are finally getting the importance of differentiation

But there's still a lot of work to do.

Developing unique features for its own sake won't cut it. Banks need to innovate with purpose.

That starts with understanding what customers expect, and delivering it in a seamless, intuitive, user-friendly way. But what ultimately sets leaders apart is that they anticipate consumers' evolving needs and address them before others can.

And that means access to complete, accurate, up-to-date digital banking research has never been more critical.

Want an in-depth, real-time view of the US digital banking landscape?

Try FinTech Insights, free, today

Build a digital banking strategy that can't be challenged

Let's show you how FinTech Insights can help you wow your customers, on every login.