Our methodology: Which card management features have we evaluated?

For our analysis, we looked at whether customers could perform the following five actions from within the apps of the banks and challengers in our sample quickly and easily, without having to call or visit an ATM or branch:

- Activate a debit card

- View or change their card's PIN

- Report a lost or stolen card

- Create a virtual card

- Create a disposable card, that is, a card with details that can only be used once

We restricted our analysis to these five specific actions for two reasons.

First, even though, in theory, it should be fairly easy to complete these tasks without leaving the app, there are still many instances where the consumer is forced offline.

Second, these features dramatically enhance the user experience, and increase security.

Our sample comprised 99 firms — 47 US incumbents and neobanks, 36 EU banks, and 16 UK banks. We focused our analysis exclusively on iOS apps.

Card management: the overall picture

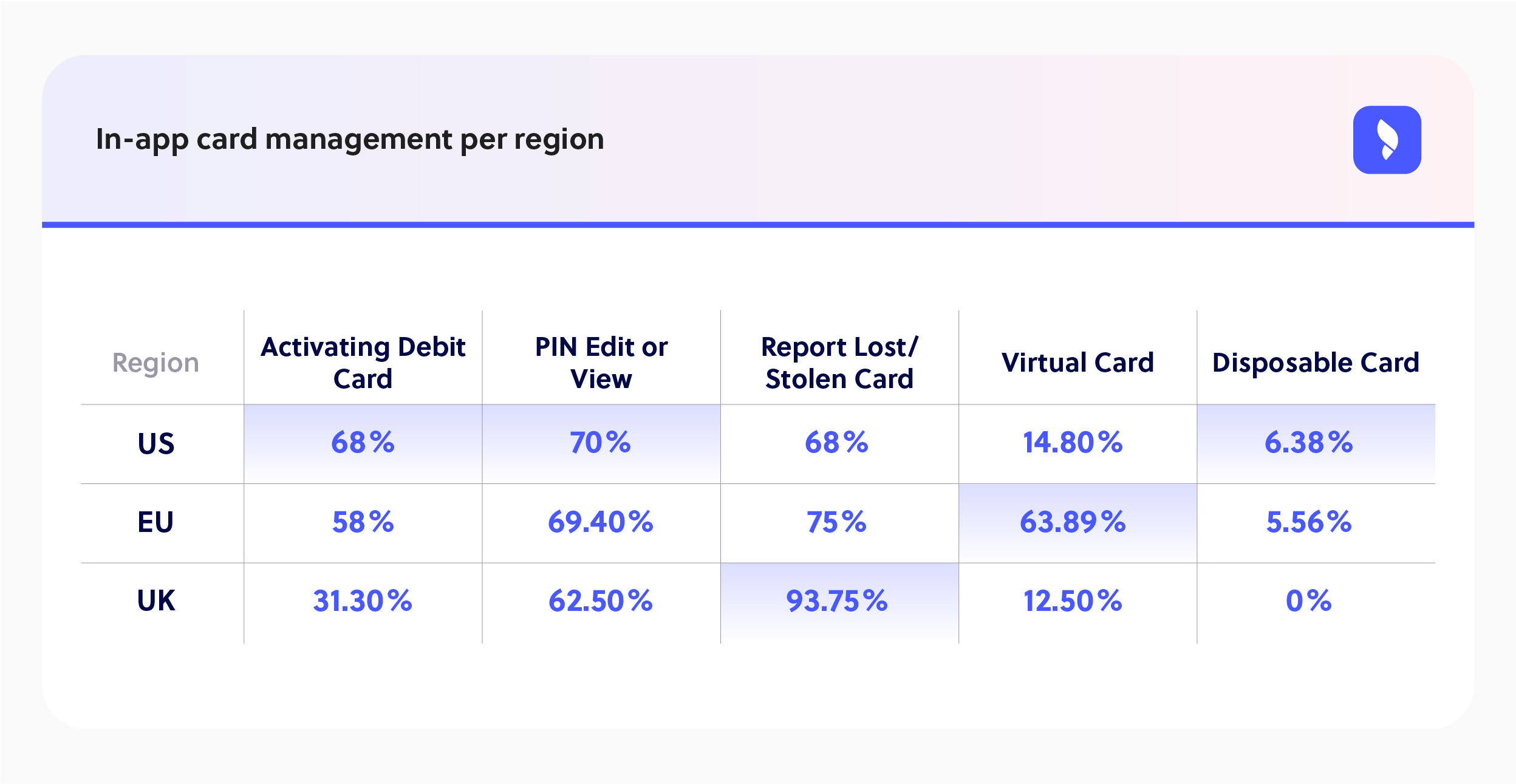

The most widely available functionality, by far, is the ability to report a lost or stolen card: 74.7% of the firms in our sample offer it.

At the other end of the spectrum, disposable cards are the most uncommon feature, with only 5% of our sample offering it.

The second, third, and fourth most common card management functionalities overall are changing or viewing the card PIN (68.7%), activating a debit card (58.6%), and creating a virtual card (32.3%) — a card which is digital only but, unlike a disposable card, has fixed details.

The geographic split: Who does in-app card management best, the US, EU, or UK?

With the exception of disposable cards, which are rare across the board — only 3 US firms (Aspiration, Bank of America, and Revolut) and 2 EU firms (Hellenic Bank and Sumeria) have the capability — no single region seems to have the edge. The US does better on some card functionalities, while the EU and UK do better on others.

The most widely available card management functionality in the US is the ability to view and edit your PIN. 70% of US firms offer it, compared to 62.5% of UK firms. In the EU, 69.4% of the sample offer the capability, only slightly lower than the US.

The US also does better on in-app debit card activation. 68% of US firms in our sample have the capability, compared to around 58% of EU firms and 31.3% of UK firms.

The EU and UK, on the other hand, do better on reporting lost and stolen cards (93.75% of UK and 75% of EU banks, compared to 68% of US firms). In creating virtual cards, the EU is the strongest, with 63.9% of banks offering the capability, compared to 14.8% in the US and 12.50% in the UK).

With the exception of The Cooperative Bank, which also lacks the other four card management functionalities we looked at, every UK bank in our sample makes it possible to report a lost or stolen card through their iOS app. EU banks that don't have the capability are similarly in the minority: 9 out of 36.

EU firms are more likely than UK firms to offer virtual cards. In the UK, only Monzo and Starling have the capability. In comparison, 23 out of 36 EU banks (63.9%) offer them.

Looking ahead: What the numbers mean for firms moving forward

The key takeaway from our analysis of in-app card management features is that there's no outright winner. US and European firms are good at different things.

But there's one area where banks and challengers on both sides of the pond have work to do: bringing digital card management more in line with consumers' increasingly mobile-first banking preferences.

Case in point, why not make it easy to activate a new card from inside the app? It's more practical, quick, and convenient. The same goes for tasks like viewing or changing the PIN, or reporting a lost or stolen card—handling these directly through the app is faster, more secure, and hassle-free.

In addition, virtual and disposable cards enhance the security of online transactions. Virtual cards add an extra layer of protection by enabling users to use them instead of their primary card. Plus, they can be easily terminated and replaced with a new one at no additional cost. Disposable cards, on the other hand, enhance the security of online transactions by being single-use. Once the customer completes a purchase, the card details can't be used again. Which means that, should bad actors get their hands on them, they'd be worthless.

With payment fraud losses expected to reach $362 billion globally by 2028, according to Juniper Research, isn't it odd that they're such a rarity?

Want to take a more in-depth look at the current state of online card management functionality in the market where you operate?

Try FinTech Insights FREE today

Build a digital banking strategy that can't be challenged

Let's show you how FinTech Insights can help you wow your customers, on every login.